|

Features

|

Vishwanadha Trust | Support to the Foundation

Viswanadha Foundation

Support to the Foundation

The Foundation accepts any donation, contribution, grant or subscription in cash

or kind, from any individual, Institution, Organization, Trust, Corporation, Company

or any other Undertaking with or without conditions towards the corpus or the income

of the Trust.

The Foundation may apply to the Government, public bodies, urban, local, municipal,

district and other bodies, companies or persons for, and to accept grant of money

and of aid, donations, gifts, subscriptions, and other assistance with a view to

promoting the objects of the Trust.

The Foundation may also discuss and negotiate with the Government Departments, public

and other bodies, corporations, companies or persons, scheme(s) and other work and

matters within the objects of the Trust, and to conform to any proper condition(s)

upon which such grants and other payments may be made.

Donations, contributions, etc to the Viswanadha Foundation can directly be credited

to the Savings Bank Account No. 6448 with the Canara Bank, Prasanthi Nilayam - 515134,

Andhra Pradesh, India. They may also be sent by way of Account Payee Cheques / Demand

Drafts / Pay Orders in favour of Viswanadha Foundation payable at Prasanthi Nilayam,

to Sri K.R.Paramahamsa, Trustee, Viswanadha Foundation, S3-B4, Prasanthi Nilayam

- 515134, Andhra Pradesh.

The Commissioner of Income Tax, Tirupati conveyed approval that the donations /

contributions made to the Trust would be allowed under Section 80 G (5) (vi) of

the Income Tax Act, 1961 in the hands of the donors, made from March 11, 2005 to

March 31, 2008. A copy of the proceedings of the Commissioner of Income Tax, Tirupati

is attached.

GOVERNMENT OF INDIA

TEL: 0877 2287541

FAX: 0877 2287531

SRI A.R. REDDY, I.R.S.

OFFICE OF THE

COMMISSIONER OF INCOMTAX,

AYAKAR BHAVAN,

K.T. ROAD,

TIRUPATI –517 501.

PROCEEDINGS OF THE COMMISSIONER OF INCOMETAX, TIRUPATI

(April 2005 to March 2008)

F. No. Hqrs I (410) /CIT / TPT / 2004-05

DATED: 28.04.05

Sub: Approval u/s. 80G (5) (vi) of the Income Tax Act, 1961- Your own - Regarding.

Ref: Your application in Form No. 10G filed on 22.03.05.

* * *

Deduction in respect of donations to your Trust / Society / Institution will be

allowed u/s. 80G (5) (vi) of the Income Tax Act, 1961 in the hands of the donors

subject to the limits prescribed therein.

2) The approval is initially valid in respect of donations received by you from

11.03.05 to 31.03.05. in the receipts issued by you, the fact that the deduction

will be available for donations received during this period only, should be clearly

mentioned.

A.R. REDDY

Commissioner of Income Tax

TIRUPATI

Conditions:

1.The receipts issued by you to the donors should bear the number and date of this

order.

2.You may submit the statement of income and expenditure and other relevant accounts

and reports within the specified time to the Assessing Officer.

3.Amendments, if any, proposed to the aims and objects shall be made only after

obtaining the prior approval of the Commissioner of Income Tax, Tirupati.

Copy to: The Assistant commissioner of Income Tax, Circle-I, Anantapur

1.His attention is drawn to the CBDT’s letter F. No.20 / 3 / 6.9 / II (A-I) dated

18-4-69. He is requested to verify and satisfy himself that the above applicant

continues to fulfill the conditions laid down u/s. 80G (5) and, if not, necessary

action may be initiated.

2. He shout keep a close watch over the activities of the Trust / Society / Institution

in future and necessary action initiated in a case of violation of or departure

from the provisions of Sec.11, 12 & 13 or the I.T. Act, 1961.

Copy to: The Additional Commissioner of Income Tax, Range Anantapur.

------------------------------------------------------------------------------

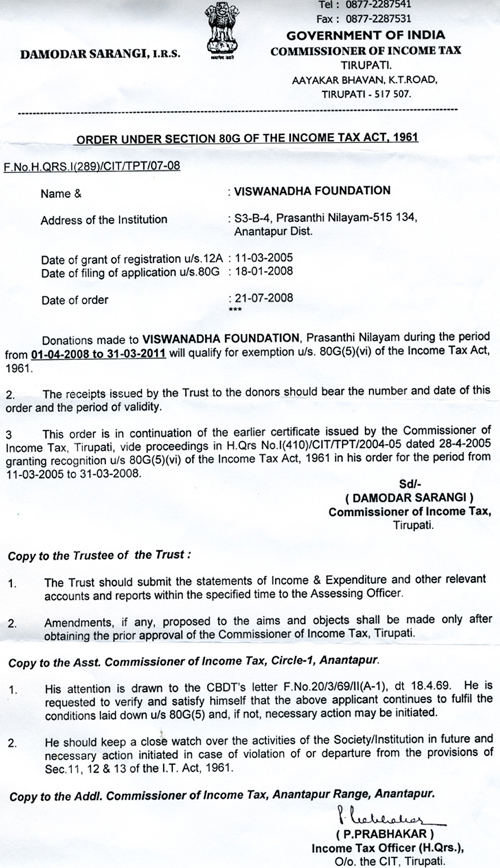

The Commissioner of Income Tax, Tirupati has renewed approval that the donations

/ contributions made to the Trust will be allowed under Section 80 G (5) (vi) of

the Income Tax Act, 1961 in the hands of the donors, made from April 1, 2008 to

March 31, 2011. A copy of the proceedings of the Commissioner of Income Tax, Tirupati

is attached.

PROCEEDINGS OF THE COMMISSIONER OF INCOMETAX, TIRUPATI

(April 2008 to March 2011)

|